Term Insurance is a familiar term. But, do you actually know what term insurance is?

Well, term insurance is the elementary baseline for any fiscal plan as it is pocket-friendly and comes with good protection coverage.

Although, term insurance is one of the basic life insurance products, there are various myths about term plans. You might be unsure about the claim settlement if you have more than one term insurance plan. Many of us baffle, whether or not they would get the best coverage.

There are many term insurance plans offered by various insurance providers. SBI term insurance plan is one of the most sought-after choices among the insurance buyers. Apart from this, there are various other providers offering term insurance policies.

So, if you’re planning to buy SBI term insurance policy, you must check the things mentioned below when buying SBI term insurance policy:

Objective:

What’s the purpose of buying a term life insurance plan? Is it tax saving or securing your family or both?

Many term insurance subscribers have a wrong notion that they can claim the entire premium paid as income tax deduction.

Is this true?

No. It isn’t.

Deductions are restricted to only 20 percent of the capital sum insured in respect to the plans issued on or before the FY ending on March 31, 2012. Moreover, 10 percent deduction is allowed in case of plans issued on or after April 1, 2012, as per the Income Tax Act, 1961.

Ascertain the Cover Amount:

You must ascertain the cover amount before buying the term plan by SBI. In order to make a wise decision on the amount of coverage, you need to assess and take a few factors into consideration. These factors are:

-

Your financial responsibilities

-

Your age

-

The future financial needs and requirements of your family

-

The basic expenses based on lifestyle habits

-

The amount of loan you’re servicing at present.

-

Whether you’re accounting for rising costs and inflation.

Ideally,

Determination of the Policy Term:

Second comes the term of the policy. This depends on your age, retirement age, and financial responsibilities.

Let’s see how:

Depending on Age:

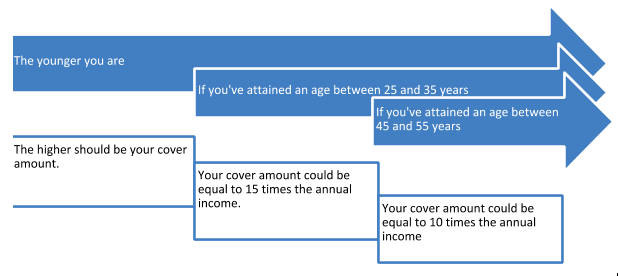

First and foremost, you can ascertain the tenure of your policy basis your age. The younger you are, the higher policy term would be recommended.

For example:

|

At the age of 20s |

40 years of the policy term is recommendable |

|

At the age of 50s |

10-15 years of policy term is recommendable |

|

In case, you’re seeking to buy a higher-cover and lower premium term policy |

It is recommended that you buy the term plan at an early age. |

Depending on while retiring:

If you’re having a retirement plan, then you can choose the policy term until you reach your retirement age, which is generally 60 years for many people. This will make sure that your cover extends throughout the working years and your loved ones are financially secure in case of any unforeseen event.

Nevertheless, if you’ve not planned for your retirement yet, you must take the term plan for the maximum period.

You can make payment of the premiums only until your retirement age that is until the time you’re earning. But the cover continues for more than an age of 60 years! Interesting, right?

Depending on other financial liabilities:

Based on your other financial liabilities and commitments and when they’re due, you can opt for the best-suited policy term. For instance, if have a loan for 30 years, this makes sense to opt for a term insurance cover for around 30 years so that your loved ones are protected from any financial trouble in case of an unforeseen event.

Pick the Right Insurance Provider:

Buying a term plan is not an easy task. Investing in insurance is a long-term commitment. Therefore, you must follow an out-and-out understanding of the product together with the information about the history of the insurance provider.

While deciding onto your insurance company, you must do some basic checks. You must familiarize yourself with their solvency ratio, claim settlement ratio, market reputation, financial background, etc.

You must choose an insurer with a high Claim Settlement Ratio and higher Solvency Ratio.

Additional Rider Benefits:

Term insurance schemes are best-suited for people looking for comprehensive risk cover against the liabilities. These plans offer additional rider benefits like critical illness cover and accidental disability/death, or the Accelerated Sum Assured. You just have to pay a little extra premium amount in order to avail these added benefits.

Risk Covered:

Before you buy a term insurance plan, you must closely observe the sum insured, benefits offered, the flexibility provided, risks covered, premium amount etc. It is also recommended that you compare the plans offered by several insurance providers before you finalise a choice.

On a Final Note!

Term insurance is surely the way to go. This article reiterates the rationale of making a well-informed decision of selecting a term insurance plan.

-

Firstly, in case of being the only breadwinner of the family, the value of your income would be secure.

-

Secondly, it would protect the financial future of your family and loved ones with higher life cover.

-

Thirdly, it is accompanied by tax benefits

After signing the dotted lines on the policy document you would have a sigh of relief on your face. Your loved ones would appreciate your investment as you got them covered on all counts!

Leave a Reply: