How APR Works on a $200 Loan

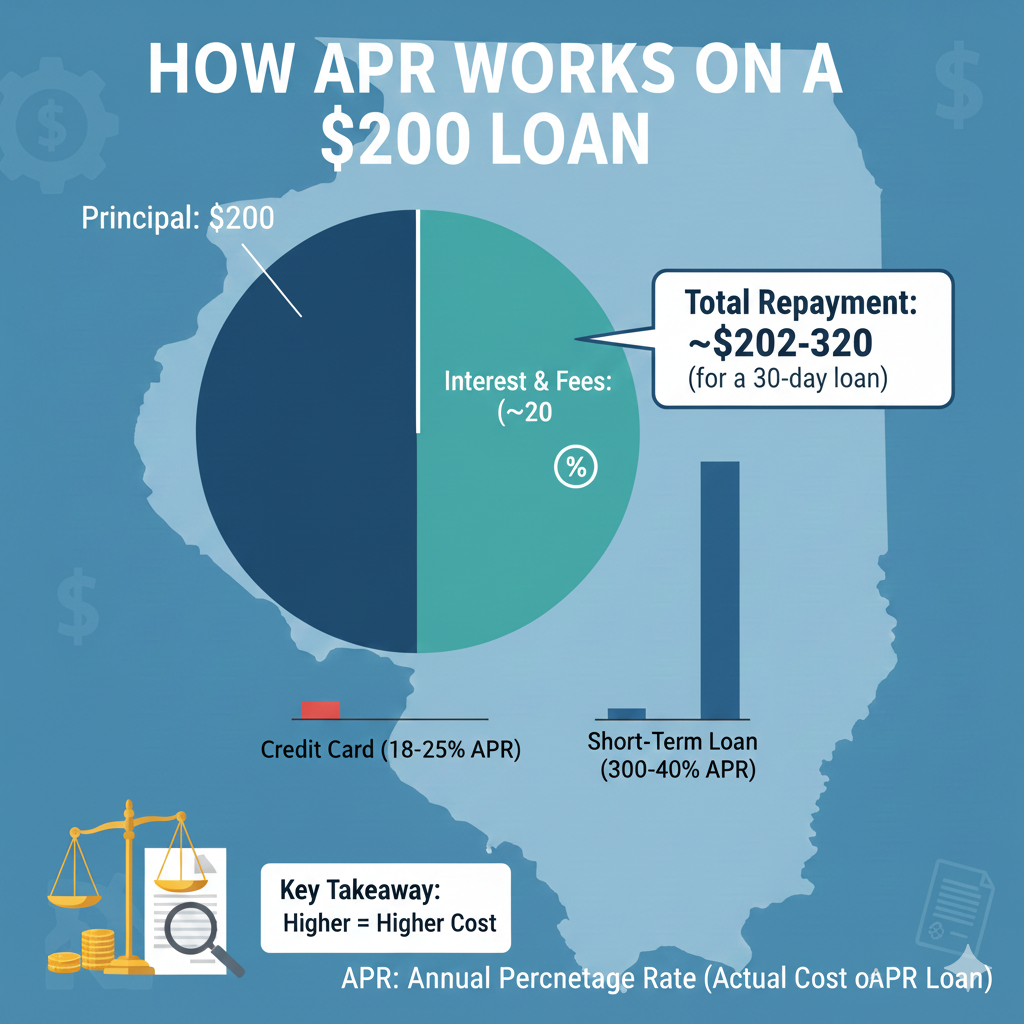

Understanding how APR works on a $200 loan is essential for making informed borrowing decisions. Because $200 is a small loan amount, even modest fees can produce a high annual percentage rate (APR). That doesn’t necessarily mean the loan is unaffordable—it simply reflects how APR is calculated over a full year, even when the loan lasts only days or weeks.

EasyFinance.com helps borrowers understand real borrowing costs by matching you with reputable, BBB-accredited lenders offering transparent terms, fast approvals, and loan amounts up to 2000 dollars. Knowing how APR applies to a small-dollar loan empowers you to choose the safest and most cost-effective option.

What APR Really Means

APR—or annual percentage rate—represents the yearly cost of borrowing, including interest and required fees. For small loans like $200, APR can appear surprisingly high because fees are annualized even though the loan may be repaid quickly.

Some borrowers first explore fast-cash options such as payday loans online no credit check, but APR always depends on the exact fees and repayment schedule—not just how quickly you receive the money.

Why APR Looks High on Short-Term Loans

The shorter the repayment period, the higher an APR will appear. For example, a lender charging a $20 fee on a $200 loan repaid in 14 days produces a high APR once annualized. However, your real out-of-pocket cost remains the $20 fee plus the $200 principal.

Borrowers comparing emergency options—including online payday loans no credit check—should always evaluate total repayment rather than just the APR figure.

How APR Is Calculated on a $200 Loan

APR includes:

- Interest charges

- Required lender fees

- Loan term (days or weeks)

- Repayment structure (single payment or installments)

If the loan term is short, the APR grows because the formula treats the fee as if it applied for a full year, even though the loan doesn’t last that long. This is normal for short-term borrowing.

For comparison, some borrowers examine slightly larger products like a same day loans online offer to see how APR shifts with different loan amounts and periods.

APR vs Total Loan Cost

APR is useful for comparing lenders, but your real concern should be the total repayment amount. With a $200 loan, small differences in fees matter more than differences in APR percentages.

For example, an installment lender charging a small, fixed fee may produce a much lower total cost than a lender offering a single-payment structure. Reviewing both APR and total repayment ensures you choose the least expensive option.

When evaluating alternatives, borrowers sometimes look at a $1,000 quick loan no credit check to compare how APR reacts when the loan size increases.

APR on Installment vs Single-Payment Loans

Installment loans spread repayment over multiple payments, typically showing a lower APR than single-payment payday loans. This is because the borrowing period is longer, even when the total cost is similar.

If you prefer structured repayment rather than a lump-sum due date, an installment plan may make the APR more manageable and predictable.

Some borrowers also explore flexible options such as tribal loans online same day, but APR disclosures vary widely, so compare carefully.

How State Regulations Affect APR

APR on a small-dollar loan can vary depending on where you live. Many states place limits on fees, loan length, and rollovers. Understanding your state’s regulations helps you predict what APR ranges are typical or permitted.

While evaluating legal frameworks, some borrowers review other fast-access products like same day loans no credit check to understand what lenders can legally offer in their state.

What Lenders Consider When Setting APR

To determine APR for a $200 loan, lenders assess:

- Your income and deposit frequency

- Bank account stability

- Loan term and repayment plan

- State fee restrictions

- Risk of nonpayment

Because small-dollar loans carry administrative costs similar to larger loans, lenders often charge flat fees, which raise the APR more dramatically on small amounts.

Borrowers comparing fast solutions sometimes also evaluate a $300 payday loan, which illustrates how APR behaves at a slightly higher loan amount.

APR and Bad Credit Borrowers

Bad credit does not automatically mean a higher APR on a $200 loan. Many lenders rely more on income verification and bank stability than on traditional credit scores.

Because of this, borrowers with challenged credit often qualify for manageable terms, similar to offers such as a $300 loan bad credit.

How to Compare APRs Across Lenders

When comparing $200 loan offers, assess:

- Total repayment amount (principal + fees)

- APR listed in the disclosure

- Repayment schedule

- Automatic withdrawal requirements

- Early repayment policies

Additionally, some lenders—such as those you might find through a tribal lenders list—may have significantly different APR structures. Always confirm terms before accepting.

APR and Risky or Unregulated Lenders

Unlicensed lenders may fail to disclose APR or use misleading language. High-risk lenders sometimes emphasize “low weekly payments” while hiding the true total cost. Always require full APR disclosure before accepting an offer.

If a lender offers a product similar to a no credit check tribal loan, verify that APR details are provided clearly and legally.

Why EasyFinance.com Helps You Find Fair APRs

EasyFinance.com works only with reputable lenders that disclose APRs transparently and follow legal lending requirements. With one secure application, you can compare offers side by side to understand which lender provides the most affordable option.

- Clear APR and total repayment disclosures

- Fast approvals and direct deposits

- No hard credit checks for many lenders

- Loan amounts up to 2000 dollars

- BBB-accredited platform for safe borrowing

This ensures you avoid high-risk lenders and choose an option that fits your budget.

Key Insights

- APR on a $200 loan appears high because fees are annualized over a short-term period.

- Your true cost is the total repayment amount—not just the APR percentage.

- Installment loans may show lower APRs than single-payment loans.

- Bad credit does not prevent getting a manageable APR on a small loan.

- EasyFinance.com helps you compare lenders and choose fair, transparent offers.

FAQ

Why is the APR so high on a small $200 loan?

APR is annualized, and short-term loans create high percentage values even when total fees are modest.

Does APR show the total cost of the loan?

APR reflects yearly cost, but always check total repayment to understand what you will actually pay.

Can I get a $200 loan with a lower APR?

Yes. Installment loans or lenders with lower flat fees can produce more manageable APRs.

Does bad credit increase APR?

Not always. Many lenders assess income and bank stability more heavily than credit scores.

How does EasyFinance.com help with APR comparisons?

It matches you with transparent lenders that clearly disclose APR, fees, and repayment terms so you can choose the most affordable option.

Explore More $200 Loan Resources

- $200 Loan: Complete Guide for Borrowers

- How to Get a $200 Loan Online Fast

- Same-Day $200 Loan: What Borrowers Need to Know

- Instant Approval $200 Loans: How They Work

- $200 Loan No Credit Check: What’s Real and What’s Not

- Guaranteed $200 Loan Offers: Are They Legit?

- Requirements for Getting Approved for a $200 Loan

- Best $200 Direct Lender Loans Online

- How to Apply for a $200 Loan With Bad Credit

- Fast $200 Cash Advance Loans Online

- How Fast Are $200 Online Loans Deposited?

- $200 Loan With Same-Day Direct Deposit

- Evening & Weekend Funding for $200 Loans

- How to Get a $200 Loan Overnight

- $200 Loan Funding Delays: Common Reasons and Fixes

- $200 Loan for No Credit Borrowers

- $200 Loan for Bad Credit Borrowers

- $200 Loan With a 500 Credit Score

- Soft Credit Check $200 Loan Options

- Income-Based Approval for $200 Loans

- $200 Payday Loan vs Installment Loan

- $200 Cash Advance vs Online Personal Loan

- Short-Term $200 Loan Alternatives

- $200 Borrowing With Line of Credit vs Payday Loan

- Is a $200 Loan Better From a Marketplace or Direct Lender?

- Are $200 Payday Loans Legal in California?

- $200 Loan Rules in Florida

- $200 Loan Regulations in Tennessee

- $200 Loan Laws in Alabama

- $200 Loan Limits in Ohio

- How $200 Loan APRs Work in Illinois

- $200 Loan Fees and Caps in Louisiana

- Legal $200 Loan Options in Georgia

- Best Places to Get a $200 Loan in New York

- Documents Needed for a Fast $200 Loan

- How Bank Verification Works for $200 Loans

- Why Some $200 Loans Get Denied

- How to Increase Approval Odds for a $200 Loan

- $200 Loan for Emergency Expenses

- $200 Loan for Car Repairs

- $200 Loan for Utility Bills

- $200 Loan for Rent or Housing Emergencies

- How APR Works on a $200 Loan

- Avoiding a $200 Loan Debt Cycle

- $200 Loan Rollovers and Extensions Explained

- Safer Alternatives to a $200 Payday Loan

- Direct Lender $200 Payday Loans Online

- Tribal Lender $200 Loan Options

- Bad Credit Friendly $200 Loan Marketplaces

- Top $200 Installment Loan Providers

- 24/7 Online $200 Loan Lenders

- Weekend Funding for $200 Loans

- Holiday Emergency $200 Loans